The U.S. General Fund—Balancing America’s Checkbook

When you take money out or put money into your bank account, your account balance adjusts accordingly. For the federal government, the U.S. General Fund performs a similar function—tracking cash activity for all federal entities.

Balancing “America’s Checkbook” is a challenging, yet critical responsibility.

Today’s WatchBlog post looks at our latest report on the General Fund and some of the challenges in auditing its accounts, including their effect on the budget deficit. In February, GAO’s Kristen Kociolek testified before Congress about federal payment processes and systems related to the General Fund. Her statements were based on our FY 2022 audit of the General Fund. Watch Kristen's opening statement below.

What is the General Fund?

The General Fund reports the government’s cash activity and balances, including deposits (cash inflows) and withdrawals (cash outflows). It also contains other important financial information, such as the amount of federal government debt and the budget deficit. These buckets of transactions are reported on Schedules—financial reports of the General Fund.

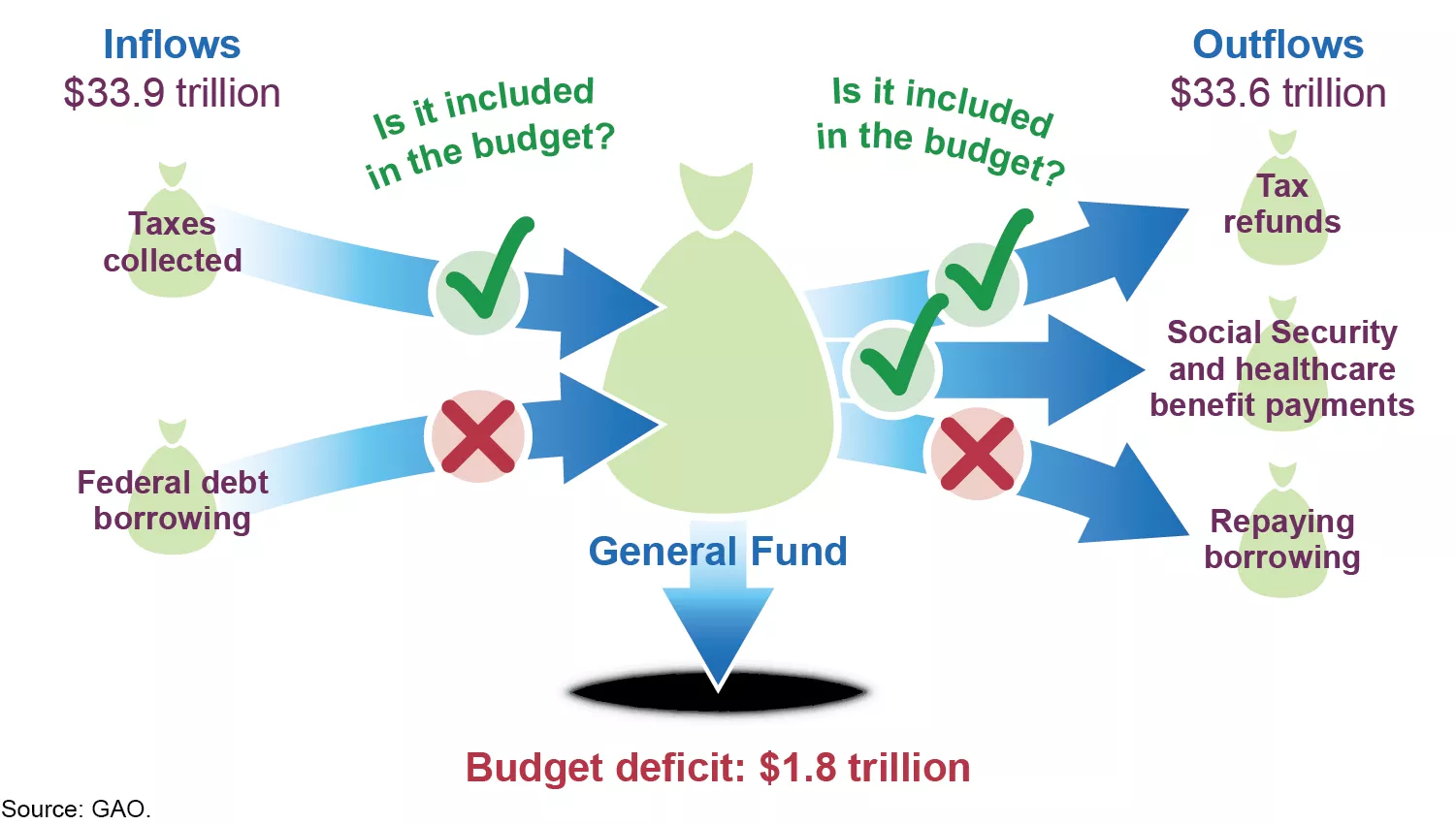

Examples of General Fund Reported Inflows and Outflows in FY 2024

Image

Most cash activity relates to federal government borrowing (about $29 trillion) and loan repayment (about $27 trillion), which do not affect the annual budget deficit. However, those inflows and outflows that do affect it, such as taxes collected and Social Security payments, can result in a budget deficit. For FY 2024, the budget deficit was $1.8 trillion.

We audited the General Fund. What did we find?

As federal government auditors, our job is to determine whether the cash activity and related account balances reported by the General Fund are reliable. When we audited the FY 2024 Schedules of the General Fund, we encountered issues that made it difficult for us to provide a clean opinion about reported amounts.

One limitation we found was that transactions are not easily tracked in enough detail as they are processed through the various General Fund IT systems. This is not a new issue. We’ve reported on this limitation since our first audit in FY 2018.

Why is it not easy to track funds? The Department of the Treasury is responsible for managing the General Fund. But we found that it is unable to easily identify and trace all transactions. This is because Treasury records transactions as a group total instead of individual balances and then processes them through a variety of systems. As a result, we did not have enough information to determine if the amounts reported are reliable, and therefore, the Schedules were not auditable.

More recently, we’ve identified additional challenges that impact the ability to clearly track funds. This includes oversight of information coming from outside entities, such as banks, that collect money on behalf of the federal government.

Does this mean cash is unaccounted for?

No. Imagine you make $200 worth of purchases at a department store, but then return an item for $50. Your bank statement might only reflect the final charge ($150) and not all of the transactions for the return. Although the record is accurate, if you were reviewing your finances months later, you wouldn’t have the details needed to understand those transactions. For the General Fund, the summarized amounts do not provide enough detail for an auditor to determine whether the Schedules are reliable.

Has Treasury made progress on the issues we highlighted?

Yes. Treasury has developed and implemented a new IT system that provides additional details for more types of transactions, giving us evidence that those entries are properly recorded. However, this solves only part of the issue, and Treasury does not anticipate resolving other issues we highlighted for several years.

Why is our audit of the General Fund important?

Transparency in government spending is important. The public’s trust in government relies on this. Taxpayers deserve to know how their dollars are being spent.

Resolving weaknesses in General Fund accounting is important because quality financial information keeps the government accountable. The transaction information from the General Fund flows to the U.S. government’s Consolidated Financial Statements, which we also audit.

The limitations identified for the General Fund affect our ability to issue an opinion on the government’s financial statements. Resolving these weaknesses is critical to ensuring high quality financial information that both keeps the government accountable and helps policymakers make sound decisions.

To read the full findings of our audit of the FY 2024 Schedules of the U.S. General Fund, see our recent report.

- GAO’s fact-based, nonpartisan information helps Congress and federal agencies improve government. The WatchBlog lets us contextualize GAO’s work a little more for the public. Check out more of our posts at GAO.gov/blog.

- Got a comment, question? Email us at blog@gao.gov.

GAO Contacts

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.