401(k) Plans: Additional Federal Actions Would Help Participants Track and Consolidate Their Retirement Savings

Fast Facts

Investing in employer-sponsored 401(k) plans is the most common way American workers save for retirement. However, people can face challenges tracking their 401(k) accounts when they transfer jobs.

Some countries use pension dashboards that allow participants to see and manage all their current and old plan savings in one place. This could be useful in the U.S., but Congress would need to authorize a federal agency to establish and oversee such a dashboard—and give it the authority to consolidate retirement account information.

We recommended, among other things, that Congress consider granting such authority to a federal agency.

Highlights

What GAO Found

The CARES Act temporarily expanded access to 401(k) retirement savings for plan participants who were impacted by the COVID-19 pandemic. GAO surveyed 14 selected companies that manage participant account data and transactions for 401(k) plans. GAO found that less than one-third of the plans covered by the surveyed companies offered the CARES Act options. Industry stakeholders GAO interviewed said larger plans and plans in industries subject to furloughs at the beginning of the pandemic, such as airlines and hospitality, were more likely to offer the CARES Act options to participants. The CARES Act options generally allowed participants to access their 401(k) plan savings in two ways in 2020:

- Participants younger than 59½ could withdraw up to $100,000 from their plan savings without facing an additional 10 percent tax for early withdrawals; they could also choose to repay the amount within 3 years.

- Between March 27 and September 22, participants could borrow up to $100,000 from their savings as a loan and delay some payments a year.

The 401(k) plans covered by the 14 companies GAO surveyed represented about 64 percent of all active 401(k) participants. Of those represented participants, GAO found that about 80 percent of them had access to the CARES Act options through their plan. Of these participants with access, 6 percent took a Coronavirus-Related Distribution and less than 1 percent took a CARES Act loan. Based on GAO's survey, the amounts of withdrawals and loans were higher during the pandemic in 2020 as compared with 2019 (see table). Industry stakeholders pointed out that workers with the greatest need for emergency funds during the pandemic in 2020—such as lower and middle-income workers—likely did not have a 401(k) plan and, thus, could not take advantage of the CARES Act options.

Comparison of Average and Median Hardship Withdrawals and Plan Loans in 2019 with CARES Act Options in 2020

|

|

2019 Hardship Withdrawals |

2020 Coronavirus-Related Distributions |

2019 Plan Loans |

2020 CARES Act Loans |

|---|---|---|---|---|

|

Average Amount |

$6,913 |

$18,344 |

$9,564 |

$33,793 |

|

Median Amount |

$3,144 |

$9,000 |

$5,097 |

$11,998 |

Source: GAO survey of 14 selected 401(k) plan record keepers. | GAO-24-103577

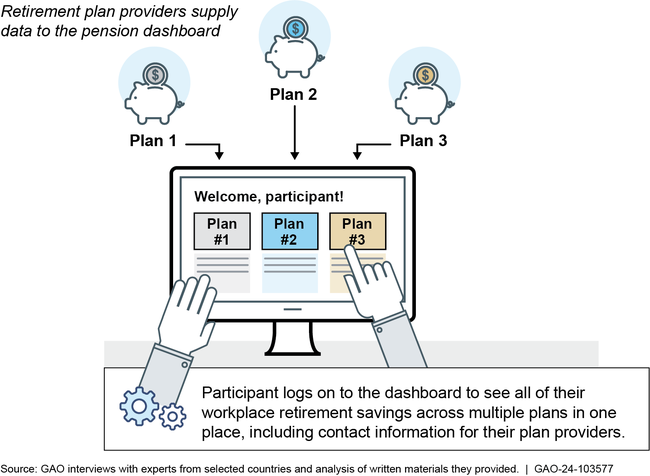

GAO also examined how six selected countries—Australia, Belgium, Denmark, the Netherlands, Norway, and Sweden—help retirement plan participants manage their savings. GAO found that all six countries use pension dashboards and other approaches to help plan participants track, manage, and consolidate their plan savings and reduce fees. For example, all six countries established a centralized pension dashboard that allows participants to view their retirement savings securely online and at no charge. According to experts from the countries, the dashboards help participants keep track of their various workplace retirement accounts as they change jobs.

Pension Dashboards Allow Participants to Track Their Plan Savings in One Place

To increase the likelihood that participants' savings will be consolidated after a job change, three of the six selected countries allow automatic savings transfers, according to experts GAO interviewed. For example, Australia, Norway, and the Netherlands allow a participant's inactive retirement plan savings from older workplace plans, to be transferred to the participant's current, active plan without the participant's consent. In Australia, plan providers must transfer savings from small inactive accounts to a government agency. The agency then holds the savings until the participant claims them, the agency transfers them to an active account, or the participant is eligible to receive the savings. Australian officials said close to 4.7 million accounts valued at $7.11 billion AUD (about $4.61 billion USD) have been reunited with participants between late 2019 and the end of 2022, helping them consolidate savings into their active accounts.

In the U.S., 401(k) participants face challenges tracking and consolidating their accounts. However, federal action could mitigate these challenges. Federal data show that more than 92 million Americans participate in and have saved more than $7 trillion in 401(k) plans. Yet, GAO's nationally-representative survey of 401(k) participants found that participants continue to encounter challenges in managing and tracking their accounts as they move from one job to another. According to GAO's survey, two-thirds of 401(k) participants would find a comprehensive pension dashboard, where they can see all of their current and old plan savings in one place, to be a useful resource. However, no federal agency has statutory authority to establish a pension dashboard.

GAO's survey also found that 401(k) participants who recently completed a plan-to-plan rollover faced challenges understanding and complying with their plans' requirements. For example, 25 percent of participants indicated that there were too many steps to follow in the process and 22 percent said they were unclear about questions or information in the rollover form. Allowing plans to automatically roll over participants' savings to their new plan after they change jobs can be beneficial for participants—particularly those unengaged with their plan—because they can benefit from account consolidation without navigating a challenging manual process. However, no federal agency has the statutory authority to establish a system to facilitate automatic plan-to-plan rollovers.

Why GAO Did This Study

Investing in employer-sponsored 401(k) plans has become the most common way for American workers to save for retirement. But plan participants can face challenges when they change jobs and with tracking their accounts. 401(k) savings can sometimes be accessed in emergencies. The CARES Act created additional options for participants to temporarily access their plan savings.

GAO was asked to review access to 401(k) plan savings during the pandemic in 2020 and challenges participants have rolling over their retirement savings from one plan to another, both abroad and in the U.S. This report examines: (1) access to and use of the CARES Act 401(k) plan options; (2) approaches other countries use to help workers track, manage, and consolidate their plan savings; and (3) challenges with 401(k) plan-to-plan rollovers and federal actions that can improve the process.

GAO's review included a non-representative survey of 401(k) companies and interviews with stakeholders representing different roles in the retirement industry about the CARES Act access options; interviews with experts from six selected countries that have: (1) a pension dashboard, (2) portable workplace retirement savings, and (3) other approaches to help workers track and consolidate their retirement savings; and a nationally-representative survey of 401(k) participants about their recent experience with plan-to-plan rollovers.

Recommendations

GAO recommends that Congress consider granting authority to a federal agency to (1) establish a pension dashboard and (2) establish a system for automatic plan-to-plan rollovers. GAO is also making four recommendations to federal agencies to help 401(k) participants, including improving the information participants receive about options for their plan savings and the process they must undergo to consolidate their savings after changing jobs.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider enacting legislation to assign and grant authority to a federal agency to establish and oversee a secure website, commonly known as a pension dashboard, that allows plan participants to view in one place information about all of their employer-sponsored retirement savings plans. (Matter for Consideration 1) | As of February 2025, Congress has taken no action on this matter. | |

| Congress should consider legislative amendments to assign and grant authority to DOL and IRS to establish an electronic plan-to-plan rollover system that, when an individual changes jobs, automatically transfers the savings from their old employer-sponsored retirement account plan to their new employer's plan (provided that their new plan accepts rollovers and that individuals can opt-out). (Matter for Consideration 2) | As of February 2025, Congress has taken no action on this matter. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Pension Benefit Guaranty Corporation | The Director of the PBGC should assess and report to Congress on the feasibility of amending current law to allow active 401(k) plans to transfer small inactive account balances subject to forced-transfers to the PBGC's program, currently known as the Missing Participants Program for terminated defined contribution plans. (Recommendation 1) |

PBGC agreed with this recommendation and initially anticipated completing a study before 2025. As of December 2024, PBGC indicated the study is underway and expects to complete it by September 30, 2025. We commend the agency's efforts and will continue to monitor its progress to implement this recommendation.

|

| Department of Labor | The Secretary of Labor should take action to implement the ERISA Advisory Council's 2016 recommendation by issuing a Request for Information to explore how the agency can encourage and support the adoption of secure electronic data standards to facilitate the processing of plan-to-plan rollovers. (Recommendation 2) |

As of April 2024, DOL indicated it is waiting for Treasury to issue guidance pursuant to SECURE 2.0 Act of 2022 section 324 before DOL can more meaningfully assess whether and how to best encourage and support the adoption of electronic data standards, including formal public engagement with stakeholders. SECURE 2.0 section 324 prompts Treasury to issue guidance in the form of sample forms to simplify, standardize, facilitate, and expedite the completion of rollovers to eligible retirement plans and trustee-to-trustee transfers from individual retirement plans. In January 2024, DOL issued a proposed regulation pursuant to section 120 of SECURE 2.0 to implement a statutory prohibited transaction exemption for "automatic portability providers" who administer programs under which an employee's retirement savings that has been transferred by their employer to an IRA can be automatically rolled over to a new employer's plan, as applicable. As part of this initiative, DOL indicated it is exploring possible standards for such providers to safeguard portability data and to promptly remedy potential security breaches. As of April 2024, DOL is reviewing comments in response to the proposal. We commend DOL's actions and maintain that an initiative to develop secure standards to safeguard data for automatic IRA-to-plan rollovers would be enhanced if conducted alongside a Request for Information for secure electronic data standards for plan-to-plan rollovers. Without continued progress towards developing secure electronic standards to facilitate efficient plan-to-plan rollovers, participants will likely continue to find the process challenging and may avoid consolidating their savings altogether. We will continue to monitor the agency's progress to implement this recommendation.

|

| Department of the Treasury | The Secretary of the Treasury should take action, such as amending the 402(f) Notice requirements and Model Notice, or providing clarifying information to the Notice to: (1) include clear information about participants' option to leave their savings in their old plan; (2) provide clearer and more concise information on each of the four distribution options and their associated tax consequences; and (3) address the timing requirements for plans to provide the 402(f) Notice, to ensure the Notice is provided to participants when they leave their job and become eligible to take a distribution. (Recommendation 3) |

Treasury stated that an update to the 402(f) Notice is currently in process and will reflect legislation and guidance issued since the last update. However, regarding the part of the recommendation that address the timing requirements for plans to provide the 402(f) Notice, Treasury stated that there is no statutory authority to require a notice to a participant upon separation from service. Our recommendation states that Treasury should take action to address the timing issue; and Treasury can seek any venue it deems appropriate, including seeking statutory authority from Congress to address the timing. Without such action, Treasury will continue to miss an opportunity to ensure that participants are receiving easily-understandable information about all distribution options-at the point in time when a participant is facing an important decision about their retirement savings. We will monitor the agency's action.

|

| Department of Labor | The Secretary of Labor should ensure that plan participants, at the time they leave their job and become eligible to take a retirement plan distribution, receive easily-understandable information about all four distribution options and their associated tax consequences. Actions that could be taken include implementing the ERISA Advisory Council's 2015 recommendation, exploring a joint-agency effort with Treasury to update the 402(f) Notice, or other steps that would help plans develop clear and concise communications to inform participants. (Recommendation 4) |

As of April 2024, DOL indicated it is engaged in joint-agency efforts with the Treasury, IRS, and the Pension Benefit Guaranty Corporation pursuant to section 319 of the SECURE 2.0 Act to review and obtain feedback from interested parties about the effectiveness of all disclosures to retirement plan participants required under ERISA and the IRC. A Request for Information was published in the Federal Register in January 2024, which includes a broad range of questions about the information that is disclosed to participants, including the format, delivery, comprehension, and retention of such information. DOL noted the agencies will review such comments in preparing a required report to Congress with recommendations for potential improvements to required disclosures. As part of that tri-agency process, DOL said it will also consider our report recommendation. Also, DOL indicated in April 2024 that it has begun implementing the directive in section 342 of the SECURE 2.0 Act, which amended ERISA to require DOL develop regulations to require retirement plans to provide advance notice to participants and beneficiaries who are permitted to take lump sum distributions. In developing regulations, and any subsequent outreach and education materials, DOL said it will take into account our recommendation that participants should receive easily understandable, timely, and comprehensive information to help them make more informed decisions when separating from employment. We commend DOL's progress in working with Treasury and IRS and will continue to monitor the agency's efforts towards implementing our recommendation.

|